Originally published at supplychainbrain.com on February 5, 2015.

The supply chain may not be glamorous, but it is a powerful indicator of the state of the economy. During the recessions of 1992, 2001 and 2008, the transportation sector was among the first to plummet, and in turn was among the fastest to recover.

So what is the supply chain sector telling us today?

We just completed our ninth annual BG Strategic Advisors Supply Chain conference, convening more than 200 of the top CEOs and investors in this market. Attendees included leaders of many of the public companies in the industry, such as UPS, FedEx, XPO Logistics, C.H. Robinson, Echo Global Logistics, Panalpina, Ingram Micro, YRCW, Heartland Express, and others. Also included were some of the largest and fastest-growing privately-held companies in the industry, such as JDA Software, GENCO and NFI. We also sampled the views of top private equity investors, as well as Fortune 500 shippers like Office Depot, Coca-Cola and Walt Disney.

Our proprietary BGSA Supply Chain CEO Survey, which we conduct every January, polled more than 140 of these supply chain leaders. Their feedback may surprise you. Here are a few highlights:

• A strong 2014 for the industry: last year, 47 percent of all attendees predicted that they would achieve growth in excess of 10 percent. However, 63 percent of them in fact achieved that target. 2014 was a year of out-performance.

• A bullish forecast for 2015: in addition, 63 percent of all attendees expected their own companies to grow at more than 10 percent. This compares favorably with 54 percent that made the same prediction last year. CEO sentiment is strong, and improving.

• Labor constraints: the most common concern expressed by CEOs revolved around finding qualified staff. Last year, 31 percent expressed this concern. This year, 44 percent highlighted it. As supply chain companies grow, the labor shortage is increasing.

• A booming deal market: 31 percent of all attendees said they were highly likely to engage in mergers and acquisitions, which represents an increase from 24 percent last year.

Attendees gained the opportunity to learn from 30 speakers across 10 sessions. Out of this conference, five big “C” themes emerged: cycling, cheap oil, consumer closeness, creativity, and consolidation.

Cycling: The Shift from Asset-Light Logistics to Asset-Based Trucking

For most of the last 30 years, asset-light logistics companies were the stars of the supply chain. They achieved the highest growth, gained the highest multiples, and were rewarded with the most market value appreciation.

Not today.

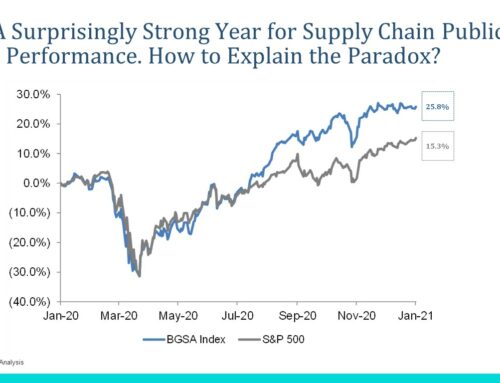

At BGSA, we track the BGSA Supply Chain Index, which is a basket of 80 companies across 9 segments, including logistics, trucking, rail, supply chain technology, and all other related segments. For 2014, the BGSA Supply Chain Index gained 17 percent, outpacing the S&P by 6 percent.

The top-performing sector was Less-than-Truckload (LTL), which spiked up by 31 percent. Rail came in as a close #2, with a 27-percent increase. The logistics basket increased by a comparatively small 8 percent. We saw a few exceptions – for instance, XPO was up 55 percent – but this was a great year for trucking, as reflected in star performances from Covenant (up 230 percent) and SAIA (up 73 percent) in particular.

Why? We see a variety of factors, including a surge in demand, capacity constraints, and the resulting supply-demand imbalance that favors carriers. Meanwhile, pricing continues to strengthen. For instance, truckload pricing is expected to increase 5 percent in 2015, versus 3 percent to 4 percent in 2014. And trucking is expected to continue to boom. For instance, December Class 8 orders were up 38 percent year-over-year, which was the fourth-best month on record.

But challenges lie on the horizon. Perhaps the biggest challenge is the driver shortage. We face a forecasted shortage of 240,000 by 2022. Why is that? For starters, not a lot of people want to drive trucks, and in good economic times, they have good alternatives. Meanwhile, let’s take a look at the data. Fifty-six percent are over the age of 45, 75 percent are obese and 87 percent suffer from hypertension. The average driver life expectancy is in the early 60s. Is it surprising?

Cheap Oil: A Double-Edged Sword

A second theme is the impact of lower-cost oil. Crude oil prices have dropped more than 50 percent since June. This disruption has had a mixed impact on the supply chain sector.

What is the impact of cheap oil? This reminds us of Harry Truman’s famous dictum: “Find me a one-handed economist!”

On the one hand, it is unalloyed good news for the economy. The oil drop is effectively a tax cut for the entire country, putting more money in consumers’ pockets that cycle through the rest of the economy. It also slashes operating costs for trucks, ships and railroads.

On the other hand, cheap oil has some negative ramifications for railroads. It lowers the expected volume of crude-by-rail transport. It also lowers the oil and gas rig counts in the lower 48 states of the United States, leading to a cut in the amount of domestic transportation associated with rigs.

Going forward, we think cheaper oil will continue to boost margins for transportation companies, and play a positive role for the industry as a whole.

Consumer Closeness

A third theme is the acceleration of direct-to-consumer.

As e-commerce increases, supply chain companies are engaged in a race to get closer to the consumer. XPO acquired 3PD to add a last-mile capability. EBay bought Shutl to create a same-day network. FedEx just purchased GENCO to gain e-commerce and reverse logistics solutions. And Amazon has announced the intent to give customers a one-hour delivery window for certain goods!

Underlying all of these moves is a commitment to reaching the end consumer.

On the one hand, low interest rates are accelerating this trend. With borrowing costs at all-time lows, companies are increasingly choosing to increase their inventory and decrease their transportation. Warehousing companies discussed their customers’ desire to shift from large distribution centers towards a broader network of small facilities. The total warehousing and inventory cost is increasing, but the transportation network is becoming faster.

On the other hand, customer service is another core driver. As one transportation CEO put it, “Our clients want us to deliver a “silent Yelp”! Supply chain companies that deliver a reliable, fast and consumer-friendly experience can become brand extensions for their customers, and in turn can become far more valuable.

The implications of this shift are immense. Winners include technologies for dynamic routing on handhelds; last-mile networks; reverse logistics solutions; companies that can shorten sourcing and delivery cycles; and other direct-to-consumer enablers.

Creativity: It’s Not Just Uber

A fourth theme is creativity and innovation. Uber is worth $40bn after just 5 years. But we see innovation throughout the supply chain.

One key driver is e-commerce. With e-commerce purchases up 20 percent year-over-year, lots of companies are emerging as winners. The obvious beneficiaries are e-commerce fulfillment companies, like eBay (which has acquired Shutl and GSI). Pure-play e-commerce companies like uShip are also benefiting. A less obvious but equally compelling winner is last-mile delivery. Companies like Grand Junction, Beavex and XPO benefit from this capability.

A derivative of e-commerce is the rise in omnichannel. Consumers want to be able to buy a product, offline or online, with a seamless experience. That requires supply chains to adapt. In the 2015 Capgemini Annual Logistics Study, 50 percent of all respondents are testing new fulfillment strategies. Only 2 percent rated themselves as high-performing in the omnichannel arena. Hence, we are seeing a spike in technology investments.

Another form of innovation lies in supply chain network design. Increasingly, companies are choosing Mexico as a manufacturing hub. Mexico has more free trade agreements than any other country, a low-cost position, and immediate proximity to the U.S. Forty percent of survey respondents have already moved some operations to Mexico. Fifty-five percent moved there from the U.S.; 36 percent from China. Key factors were reduced transport time and proximity to sources. As one CEO put it, “Mexico is no longer just about cheap parting. We are seeing real integration between the Mexican and U.S. supply chains.” Companies are using Mexico as a part of their holistic strategy, including quality control, final assembly, exports and other core services. This is creating geographic ripples, and benefiting companies that can take advantage of multinational markets.

Consolidation: The Party Continues

The fifth and final theme is consolidation. Amidst all of these positive catalysts, we are witnessing perhaps the strongest financial markets we’ve ever experienced.

On the deal side, the M&A markets are at record levels. Across the U.S. economy, M&A volume reached $1.6tr in 2014. This represents a 43-percent increase over 2013, and is in fact the highest activity level on record. IPO volumes are also at comparable levels. In 2014, $96bn was raised across 293 deals, representing the highest level since 2000.

Within the supply chain sector, the deal and capital markets are booming. Smart companies are taking advantage of this opportunity. On the acquisition side, C.H. Robinson bought Freightquote, marking its largest brokerage acquisition to date. XPO has bought 13 companies, including New Breed, its largest deal to date, and a move that takes them into contract logistics. XPO is also using the capital markets shrewdly, raising $700m from three sovereign wealth funds in September, and building a war chest for additional deals.

All of these plot lines will continue to develop over the course of 2015.

Conclusions

Going forward, we believe the growth in the supply chain sector is a bullish sign for the broader economy. The back-of-the-house successes are fueling front-of-the-house glory. While technology companies are capturing the headlines, the underlying transportation, logistics and infrastructure is poised for another year of growth.