Originally published in Logistics Management.

XPO said that its board of directors has authorized a review of strategic alternatives, which includes the possible sale or spin-off of one or more of its business units. And it added that there is “no assurance of any specific outcome” and there is no specific timetable for the completion of the review process or which, if any, of its business units would be sold or spun off.

By Jeff Berman, Group News Editor · January 16, 2020

Going back to its inception in 2011, Greenwich, Conn.-based XPO Logistics, a provider of global freight transportation and logistics services, made it clear it would build up and increase its market presence across myriad geographies, verticals, and modal offerings in the form of a growth by acquisition strategy, which quickly made the company a force in the markets it serves. In recent years, though, XPO’s acquisition activity has cooled, and late yesterday it said there is a possibility XPO may shift to selling mode after years of being a buyer.

XPO said that its board of directors has authorized a review of strategic alternatives, which includes the possible sale or spin-off of one or more of its business units, with the exception of its North American less-than-truckload unit, which is second in profit behind Old Dominion Freight Line (ODFL) and third in revenue behind FedEx and ODFL. And it added that there is “no assurance of any specific outcome” and there is no specific timetable for the completion of the review process or which, if any, of its business units would be sold or spun off.

During its nearly ten-year existence, XPO has made myriad significant investments, with perhaps the two most high-profile ones coming in 2015, when it brought both Lyon, France-based 3PL Norbert Dentressangle SA into the fold for $3.53 billion to boost its European presence, and Con-way in September 2015 for $3 billion, which made it one of the top LTL providers in North America and also expand its global contract logistics, managed transportation and freight brokerage businesses. Since Jacobs took the helm and established XPO, the company made 17 acquisitions between March 2012 and October 2015.

In an interview with LM, Jacobs explained XPO Logistics is exploring possible sales or spin-offs for four of its business units: European Supply Chain; North American Transportation (minus LTL), Supply Chain for the Americas and Asia Pacific.

“We do not intend to sell our North American LTL business, given the growth trajectory and because we believe that LTL as a standalone company would be well understood if properly valued,” he said. “We have a fantastic track record of creating tremendous shareholder value, and we think this process we are undertaking could be a way to create more value this year. We are proud that we are the seventh-best performing stock in the Fortune 500 over the last decade. Our stock is well up more than ten times since we started XPO in 2011, and we added $2 billion in revenue and have grown $500 million in EBITDA since 2015 with no acquisitions whatsoever. That said, we are trading well below the value of the sum of our parts and at a significant discount to our pure play peers. The multiples we are getting are just too low, and we believe that this discount is because currently Wall Street favors pure plays, and we have a diversified business model.”

And Jacobs added that XPO has always been intensely focused on creating shareholder value, citing the company’s $1.9 billion share buyback at $53 per share in 2019 as an example. Another example he identified was how when XPO bought an “out of favor” Con-way in 2015 and subsequently doubled its EBITDA for the sale.

“We believe the next big leg up could be considering these sales or spinoffs,” explained Jacobs. “We think there could be strong demand for each of the four businesses that we are considering selling or spinning, because all of them are top three leaders in their space powered by cutting-edge technology that XPO is so well known for. They are all performing well and have great management teams and are right-sized to be of interest to a very large number of potential buyers. That said, we will only pursue a transaction if it will maximize value beyond what we can do ourselves. We may sell or spin or one, two, three, four or no business units. But we are very excited about this process and the value that we think we can create from it.”

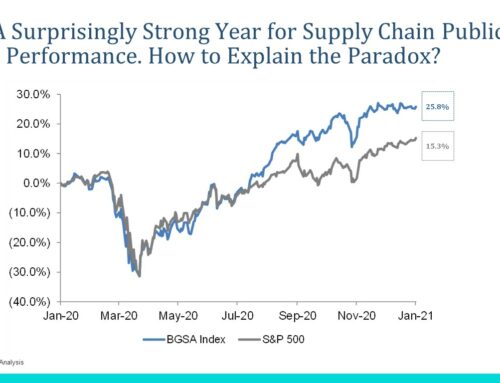

Ben Gordon, Managing Partner of Cambridge Capital, an investor in niche supply chain leaders and also Managing Partner of BGSA Holdings, a leading mergers and acquisitions advisory firm focused on the transportation, logistics, and supply chain technology sectors, said Jacobs has had legendary success pursuing acquisition-led growth.

“He scaled up prior companies including United Waste and United Rentals via deals. He then scaled up XPO with 17 acquisitions or investments,” said Gordon. “Normally Brad has been a buyer, not a seller. That said, he expanded XPO (originally Express-1) from expedited to intermodal to truck brokerage to contract logistics to less-than-truckload to truckload and more. It’s not surprising that some of the pieces proved to fit together better than others.”

Gordon added that it is likely Jacobs looks at the fact that XPO trades at 9.3 times EBITDA and thinks the company is undervalued. By comparison, he explained that CH Robinson trades at 12.5x EBITDA, Expeditors trades at 14.8x EBITDA, UPS trades at 15.6x EBITDA, and FedEx trades at 16.3x EBITDA.

“If XPO were to divest a division it considered non-core, the market could respond favorably,” noted Gordon. “Lastly, Brad might view a divestiture as a way to pay down debt and strengthen his balance sheet. For all of those reasons, I can understand why XPO is considering these strategic alternatives for a business unit.”

Evan Armstrong, president of supply chain consultancy Armstrong & Associates, had a different take on the situation, claiming that XPO is floundering strategically.

“Of all the business units, the one that has been and continues to be a mismatch to XPO’s third-party logistics business is its domestic LTL trucking operation,” said Armstrong. “It is hard to cross sell asset-based LTL trucking in conjunction with 3PL services such as Value-added Warehousing and Distribution (VAWD), and non-asset based Domestic Transportation Management (DTM) and International Transportation Management (ITM). In addition, its LTL operations are primarily B2B focused and not well suited to meet the demands of growing B2C E-Commerce market. While it could sell of its last mile operations for a solid multiple of around 10x EBITDA, it wouldn’t make sense with e-commerce 3PL market revenues growing at a compound annual growth rate of 18% according to our estimates. By comparison LTL is a slow growth market. Its VAWD operations can also benefit from the e-commerce boom. XPO Global Forwarding, its ITM business unit, could also benefit from more strategic emphasis and seems to be missing out on the e-commerce growth seen by some of its competitors. It will be interesting to see what direction XPO and its outside investment advisors take it in. Will they construct a short-term gain, or develop a long-term market-driven strategy?”